To address the deficits in the realisation of rights, the United Nations (UN) General Assembly agreed on a plan for a fairer and more sustainable future by 2030 and outlined the SDGs with associated targets and indicators. The SDGs are grounded in international human rights law, and here, we use the terms SDG progress and child rights interchangeably [4]. Governments agree that sustainable financing using domestic revenue is required to achieve the SDG agenda. However, SDG progress is off-track, in part, because of constrained government finances [5], and many countries, especially in sub-Saharan Africa, will not reach SDG targets by 2030 [6], partly because of these financing constraints.

Government revenue, child rights, governance, and the Sustainable Development Goals

Reducing losses from public finances leads to increased spending across public services in multiple sectors, such as education, agriculture, and infrastructure, which impacts children’s rights and drives SDG progress [7,8,9,10,11]. Tax is the primary means of implementing the SDGs, as most government income is derived from taxation [12]. However, tax gaps—the difference between actual collection and potential—mean that revenue is insufficient to achieve child rights. This holds particular salience for lower-income countries, whose spending on social sectors, as a proportion of the budget, is larger than that in higher-income countries [13, 14], and the gains in terms of SDG progress from marginal increases in revenue would be more substantial [15]. Thus, small revenue increases result in significant increases in coverage of SDG indicators, and thus it is critical to tackle tax-motivated illicit financial flows.

Tax gaps are comprised of both domestic and international components. Domestic tax gaps could be reduced by increasing domestic resource mobilisation, and international tax gaps could be reduced by curtailing global losses [16]. Corporate tax from multinational companies is an essential source of government revenue, especially in lower-income countries [17]. The international tax gap is mainly due to corporate tax evasion and avoidance, and in the context of a narrow tax base, curbing this is the most feasible way to fund the SDGs in the short term [18, 19]. Thus, curtailing tax gaps is essential to increasing fiscal space, which would reduce the use of regressive tax policies to raise revenue and reduce debt accumulation to cover shortfalls in national budgets [20].

Alongside revenue, governance impacts SDG progress, and government spending achieves better results in well-governed countries [21, 22]. Well-governed countries are more likely to encourage business sector development and investment, enjoy economic growth [23, 24], and have robust institutions and political stability [25, 26]. Thus, the impact of any additional government revenue is significantly amplified in well-governed countries, especially when revenue is scarce [27]. Indeed, there is a two-way relationship between government revenue and governance, which drives a virtuous circle and improves the generation of further revenue and the allocation and efficient use of additional resources [15].

The risk of illicit financial flows

The ability of governments to finance development is undermined by illicit financial flows that cause revenue losses. Illicit financial flows—“financial flows that are illicit in origin, transfer, or use, and that cross country borders”—are facilitated by jurisdictions that offer secrecy or lower or zero tax rates to residents and companies operating in other countries [23]. This problem is acknowledged in the SDG agenda. For example, target 16.4 of the 16th SDG aims to reduce illicit financial flows significantly [28]. This is the first globally agreed target to curb illicit financial flows, acknowledging the cross-border impact of national tax and financial policies and laws.

The importance of tackling illicit financial flows to increase the fiscal space for self-financed sustainable development was elevated following the establishment of the High Level Panel on Illicit Financial Flows from Africa, which was mandated by the African Union Commission and the UN Economic Commission for Africa Conference of African Ministers of Finance, Planning, and Economic Development in 2011 and chaired by Thabo Mbeki, former South African president. This informed the development of the SDGs as well as the UN’s adoption of the Addis Ababa Action Agenda, including commitments to address illicit financial flows as part of financing development [29]. According to the High Level Panel’s landmark report, often referred to as the Mbeki Report, published by the panel in 2015, commercial practices, including tax abuse, are the primary drivers of illicit financial flows from Africa, followed by criminal activities and corruption [23]. The four types of illicit financial flows can be distinguished from each other based on motivation and include 1) market/regulatory abuse, 2) tax abuse, 3) abuse of power, including theft of state funds and assets, and 4) proceeds of crime [12]. These flows sit on a spectrum of legality; some are clearly illegal, such as laundering the proceeds of crime and theft of state funds, while other transactions may be considered legal, such as instances of tax avoidance, at least when they have not been challenged in court [12]. The commercial category, or tax-motivated illicit financial flows, reduces government revenue and resources for public services. These include tax avoidance and evasion. Tax avoidance is the practice of minimising tax bills by taking advantage of loopholes or interpreting a tax code in an unintended way. In contrast, tax evasion intentionally defrauds revenue authorities. Both have the same harmful effects on government revenue.

Annual tax losses have been estimated at US$483bn worldwide due to cross-border tax abuse by multinational companies and offshore tax evasion [30]. The vulnerabilities that enable these tax losses are primarily created by member countries of the Organisation for Economic Co-operation and Development (OECD), some of which are former imperial powers and the wealthiest nations in the world, all of whom, with the exception of the USA, have ratified the United Nations Convention on the Rights of the Child [31]. Specific economic channels—exports and imports, inward and outward foreign direct investment, portfolio assets and liabilities, and banking claims and liabilities—and particular bilateral relationships between countries, especially with tax havens, increase the vulnerability and exposure of countries to illicit financial flows [32]. In Africa, Abugre et al. found that European dependent jurisdictions, and especially the UK’s crown dependencies and overseas territories, provide a disproportional share of risks of illicit financial flows in Africa across the economic channels [32].

Tax abuse and child rights

National and international obligations for children’s economic and social rights (child rights), including rights to clean air, safe water, sanitation, nutritious food, and education, are enshrined in the most widely ratified human rights instrument, the United Nations Convention on the Rights of the Child (UNCRC). All countries that have ratified the UNCRC have responsibilities for children in other countries alongside their domestic obligations. This responsibility includes promoting international cooperation to realise children’s rights everywhere and accounting for the needs of lower-income countries [33]. Although countries are generally considered primarily responsible for respecting, protecting, and fulfilling their children’s rights, they are often hampered in their efforts to meet these obligations and raise revenue to finance rights, in part because of the dynamics of international finance, trade and tax. The UN Committee on Economic Social and Cultural Rights’ General Comment Number 24 clarifies that states are responsible for the action of companies, including banks domiciled on their territory [34]:

States Parties are required to take the necessary steps to prevent human rights violations abroad by corporations domiciled in their […] jurisdiction […] without infringing the sovereignty or diminishing the obligations of the host States under the Covenant.

Here, international human rights law assigns duties to states, not companies, and international tribunals rarely extend jurisdiction over legal persons, including companies.

Since at least 2014, UN human rights experts and committees have made comments on the implications of cross-border tax abuses on human rights [35]. For example, in 2020, in their concluding remarks on the review of Ireland, the UN Committee on the Rights of the Child [36] demonstrates the connection between domestic tax policy and the impact globally on child rights,

Ensure that tax policies do not contribute to tax abuse by companies operating in other countries, leading to a negative impact on the availability of resources for realising children’s rights in those countries. (para 10c)

This is the first time that the UN Committee on the Rights of the Child has considered the effect of a country’s tax policies on children’s rights overseas. In 2022, the committee made similar concluding remarks on the review of the Netherlands [37]. Thus, international human rights law has specifically established that jurisdictions have extra-territorial responsibility for the impact of their rules and legislation that enable cross-border tax abuse because they undermine fundamental rights, including women’s and children’s rights.

Child rights in Malawi

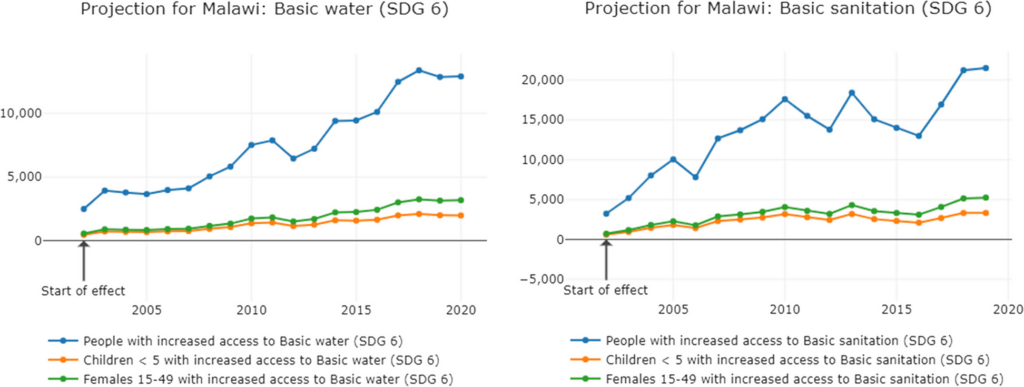

Malawi has made considerable progress in child rights, and since 2000, under-five mortality has plummeted from 172 per 1000 live births in 2000 to 39 per 1000 live births in 2020 [38]. However, there are huge gaps in children’s access to fundamental rights. For example, one-quarter of Malawian children do not have access to basic water, half do not access basic sanitation, and one-third are stunted, indicating chronic malnutrition [39]. Although 90% of children enrol in primary school, only one-third complete it [39]. On an index of SDG achievement, which measures progress towards all 17 goals as a percentage, Malawi scores 53% and ranks 145th out of 163 countries in 2022 [40]. There is a high risk that the impacts of climate change will slow SDG progress, and in particular affect children in Malawi, where Malawian children are among children from 40 countries most vulnerable, according to UNICEF’s Children’s Climate Risk Index [2]. At the population level, an increase in revenue has been shown to increase government expenditure on public services, and as a result, it will have a positive impact on health determinants and educational outcomes [31]. Of course, at the individual and household levels, there are many different factors that determine health and educational outcomes, including socio-economic circumstances and inequities [28, 41, 42].

Public finance and illicit financial flows in Malawi

The fiscal space in Malawi is limited. Government revenue as a percentage of Gross Domestic Product (GDP) is 12.6% (excluding grants) [43]. GDP per capita is $394 2015 USD [38], therefore, government revenue per capita was $50 2015 USD in 2020 [44]. Until recently, donors had contributed 40% to the national budget in Malawi (called budget support), but some donors halted this in 2013 due to the misuse of public finances, and budget support decreased to 15%. Donors redirected their support to programmes (especially in education and health) outside the budget, but this support has been criticised for poor coordination and duplication [45, 46]. Given the reorientation of official development assistance away from budget support, the government assumes that the country’s development will depend mainly on domestic resources [47], and self-reliance is the longer-term policy aim as outlined in Malawi’s Vision 2063 [48]. The government has relied on borrowing to compensate for fiscal imbalances resulting from the reduction in aid. Consequently, Malawian debt increased from 30% to 50% of GDP between 2011 and 2020, of which 20% is non-concessional external debt, and it is projected to increase to 85.7% of GDP in 2026 [49, 50]. Unless restructuring occurs, about one-third of the government’s revenue (excluding grants) will be allocated to servicing debt over the next few years [51], adversely affecting revenue allocation to child rights and all the SDGs.

The Government of Malawi’s policies to increase public finances and effectiveness include tackling different forms of illicit financial flows, driven by commercial, criminal and corrupt practices. The Malawi Revenue Authority singles out the prevention of tax avoidance and tax evasion in its Domestic Revenue Mobilisation Strategy 2021–2026 [52] and the Financial Intelligence Authority’s most recent national assessment demonstrates action on the three drivers of illicit financial flows [53].

In 2022, the Government of Malawi through the Ministry of Finance along with the African Union Commission and the Coalition for Dialogue on Africa assessed Malawi’s progress on implementing the recommendations of the aforementioned Mbeki Report. It notes that Malawi has a fairly robust legal and regulatory framework. However, effective implementation is curtailed by inadequate resources, weak coordination between institutions and political interference. The lack of cooperation from partner countries is a further limitation [54]. UNCTAD is currently piloting six methodologies to support the 2030 Agenda for Sustainable Development by defining, measuring and disseminating statistics on illicit financial flows; Malawi is not yet among the African countries where methodologies are being piloted [55]. The Illicit Financial Flows Vulnerability tracker, published by the Tax Justice Network, based on the work of Abugre et al. in 2019 [56] and building on analysis in the Mbeki Report, demonstrates the channels where Malawi is most vulnerable to illicit financial flows; on average, between 2009 and 2019, these include inward and outward foreign direct investments alongside inward portfolio investment and imports, which suggest that Malawi is at risk of tax avoidance, trade-based money laundering, and tax evasion, although it is not possible to determine the specific types of illicit financial flows without transactional level data [57].

Based on the cases investigated and/or prosecuted between 2013 and 2017, the Financial Intelligence Authority identified just over US$17 million as the total amount of corruption-related proceeds [53], which includes prosecution following a period of large-scale theft of public money popularly known as Cashgate, “although the number of identified and investigated money laundering cases may not give an accurate and full-scale picture of the threat”. Their estimates for the same 5-year time period including undetected and unrecorded proceeds from criminal offences were as follows: US$46 million for illegal possession of protected species, US$30.5 million for illegal logging, US$27.6 million for illegal externalisation of forex, US$20.9 million for tax evasion, US$18.7 million for corruption, and US$1.5 million for smuggling [53]. These amounts averaged out on a yearly basis are smaller than estimates of tax abuse, and they form just one part of Malawi’s entire burden of illicit financial flows.

There are a few case studies, generally commissioned by non-governmental organisations, that seek to quantify the revenue losses associated with multinational corporations with subsidiaries in Malawi. Most studies have focused on the tax practices of Paladin Energy which until 2020 held a mining licence for Malawi’s largest mine, Kayelekera Uranium Mine, through majority shareholding in Malawian subsidiary Paladin Africa Ltd. It was the largest single foreign direct investment at the time. In a 2015 study by ActionAid International, the organisation stated that across 6 years Malawi lost US$43 million as a result of tax breaks awarded in the mining development agreement (US$15.63 million) and of lower withholding taxes owed in Malawi through the company’s use of double tax treaties (US$27.5 million) [58]. Etter-Phoya and Malunga’s 2016 economic model of the mine concurred with foregone revenue totalling US$15 million as a result of tax incentives across five years of production [59]. Earlier studies exist, but they do not make their financial modelling explicit and made assumptions before production was suspended, such as one that estimated total annual losses of US$15 million [60]. Other multinationals, such as Malawi Mangoes, have come under media scrutiny for their tax arrangements and the potential impacts on tax revenue in Malawi [61]. However, the Malawi Revenue Authority does not systematically publish data on tax avoidance and evasion cases investigated and successfully concluded [62].

Inevitably, given their opacity, quantifying the scale of illict financial flows in any country, including Malawi, is complicated. The best data available is for tax-motivated illicit financial flows, which, according to the Mbeki Report, form the bulk of illicit financial flows, although there is variation from country to country. For these reasons, and given the cross-border obligations under international human rights law regarding tax policy, data on tax losses is the focus of the present study.

To illustrate the international community’s opportunity to contribute to SDG progress, and child rights in other countries, we use estimates of cross-border tax abuse, based on corporate profit shifting and offshore wealth. We previously presented the impact of tax abuse on SDG progress in multiple countries [31]. Here, we focus on both corporate and individual tax abuse in one country to allow us to consider domestic actions which this country (and others also) could consider to protect children from the impact of cross-border tax abuse.

We present current estimates for cross-border corporate and individual tax abuse in Malawi and the potential for increased government revenue equivalent to lost revenue in terms of SDG progress. We focus on Malawi because Malawi’s SDG progress is uneven and it was the southern African country most impacted by the war in Ukraine, with respect to its economic growth. Malawi’s revenue as a percentage of GDP declined between 2019/2020 and 2020/2021 and curtailing illicit financial flows would contribute to SDG progress by increasing government revenue [63]. Progress is further hampered by climate change [2], debt distress [64], and dwindling overseas development assistance [65], which underlines the importance of capturing lost revenue. Further, additional revenue in lower-income countries, such as Malawi, has significant impact on SDG progress. Finally, and most importantly, the authors are familiar with the domestic policy context for both child rights and illicit financial flows.

Source link : https://bmcpublichealth.biomedcentral.com/articles/10.1186/s12889-023-16319-x

Author :

Publish date : 2023-11-16 08:00:00

Copyright for syndicated content belongs to the linked Source.