SURVEY RESULTS AND DISCUSSION

BENEFITS OF THE SANDBOX TO FINTECH PARTICIPANTS AND CONSUMERS

Respondents were asked whether they saw any benefits to fintech consumers from the sandbox’s establishment. All respondents believed the sandbox would be of immense help to both participants and consumers of fintech because the platform provided a controlled environment to conduct tests under the auspices of the regulator.

UNDERSTANDING THE PURPOSE OF THE SANDBOX

Respondents were asked whether they understood the concept of a regulatory sandbox. All respondents indicated that they understood the definition of a sandbox and its purpose.

DIFFERENCE BETWEEN A REGULATORY SANDBOX AND AN INNOVATION HUB

The participants were asked whether they believed a regulatory sandbox differed from an innovation hub. All participants thought a regulatory sandbox and an innovation hub were the same.

Participants indicated that they understood the benefits of the regulatory sandbox. However, there is some doubt because none of the survey participants knew the difference between innovation hubs and regulatory sandboxes and because there is currently minimal information in the public domain regarding the regulatory sandbox project. Generally, innovation hubs provide a platform to exchange knowledge and informal guidance, while regulatory sandboxes require the involvement of the authorities. The confusion regarding the definitions implies that the RBZ should explain to participants how these elements are different but not mutually exclusive.

While there is some information regarding the objectives and intended benefits of the sandbox on the RBZ website, and the bank makes periodic pronouncements through monetary policy statements, there has been almost no information shared with consumers of fintech in the public domain; social media and traditional communication platforms could be used to improve understanding of the scheme for fintech firms and consumers of fintech.

It has been noted that transparency and quality communication could potentially increase the attraction of digital innovations to investors, allowing them to assess their investment risk more accurately because of the sandbox. However, adapting existing legal and regulatory frameworks to innovations—often across different ministries, departments, and agencies—can be overwhelming. There is, therefore, an urgent need for market-wide communication to all stakeholders if the regulatory sandbox is to achieve its objectives. The RBZ recognizes this critical need in its recommendations for a new NFIS, or NFIS II, stating that “there is a need to come up with a detailed budget to support financial inclusion initiatives such as financial literacy and consumer awareness campaigns.”16 Tunyathon Koonprasert and Ali Ghiyazuddin Mohammad have made similar observations regarding the need for quality communication between regulators and stakeholders.17

MONITORING OF DISRUPTIVE TECHNOLOGIES

Respondents were asked whether they believed the sandbox would assist the RBZ in monitoring fintech developments (“Yes”), believed the sandbox would not be helpful for this task (“No”), or had no idea either way (“No Idea”). As shown in figure 2, 69 percent responded “Yes,” 25 percent responded “No,” and 6 percent had “No Idea.”

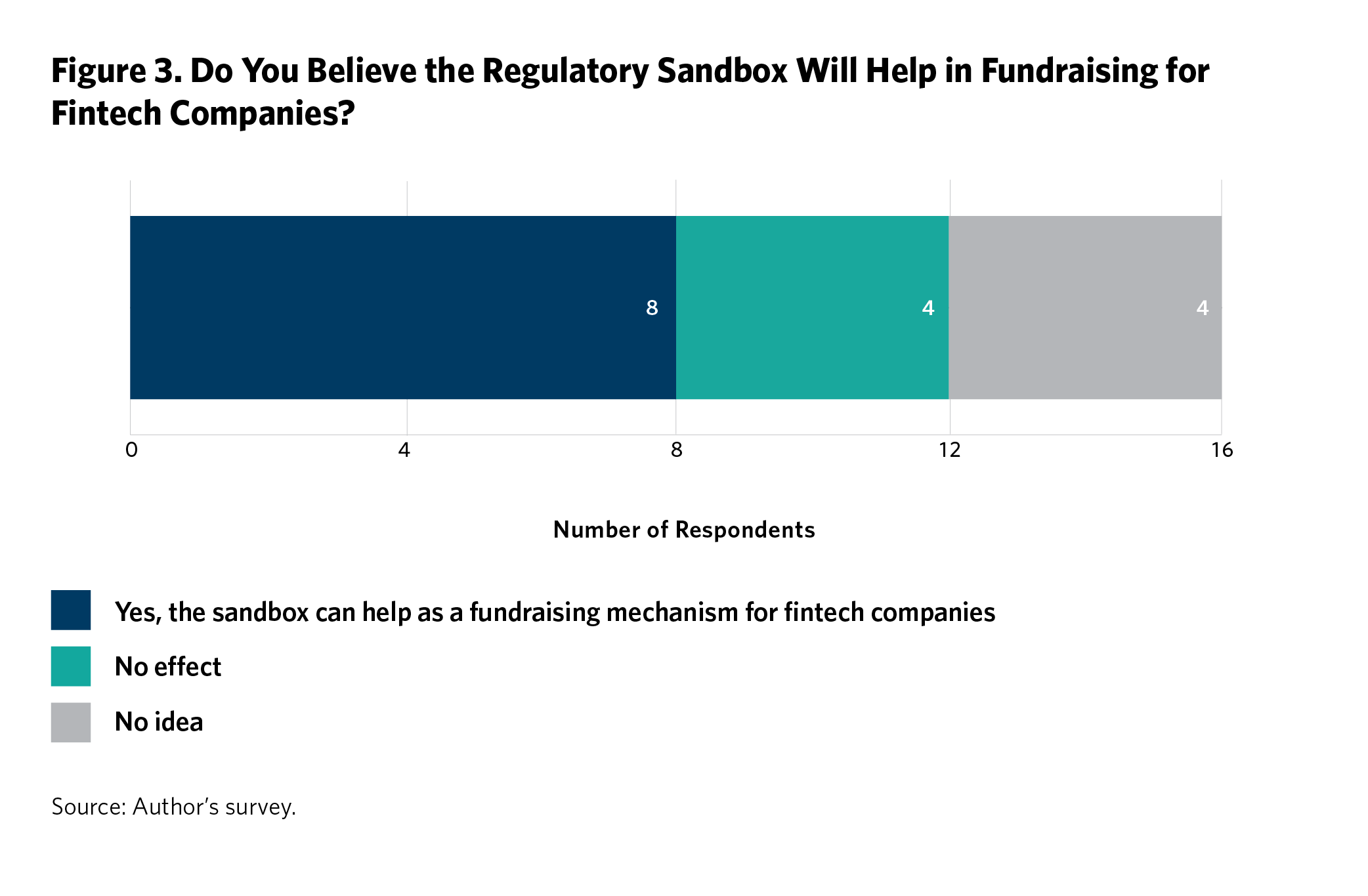

FUNDRAISING AND FUTURE GROWTH

Respondents were asked whether they believed that the sandbox would assist their organizations in fundraising for their innovations or that this was of no effect. Half of the respondents thought that the sandbox could be helpful in fundraising for their creations, while the remainder were evenly split between saying it would have no effect and saying they had no idea (see figure 3).

According to the list of possible benefits identified by the RBZ, assisting companies in fundraising is not one of the objectives of the sandbox. In other markets, participants have leveraged their sandbox participation to attract venture capital companies for funding; if the participants in the RBZ’s sandbox are unaware of this potential, this could be a missed opportunity.

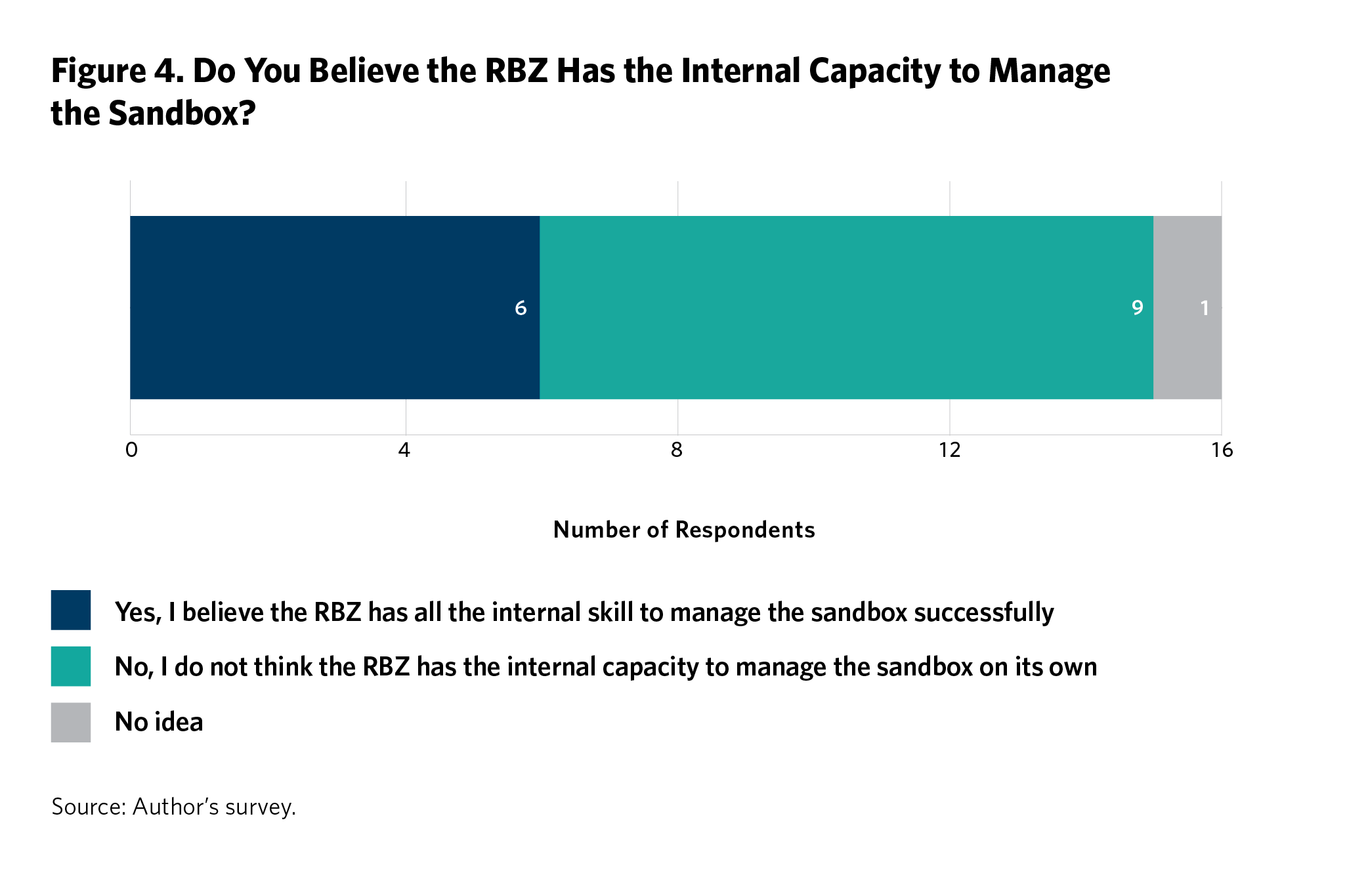

INTERNAL CAPACITY AT THE RBZ

Respondents were asked whether they believed the RBZ had enough resources to manage the sandbox. Most participants thought the RBZ lacked the internal skills to handle the sandbox successfully, as shown in figure 4.

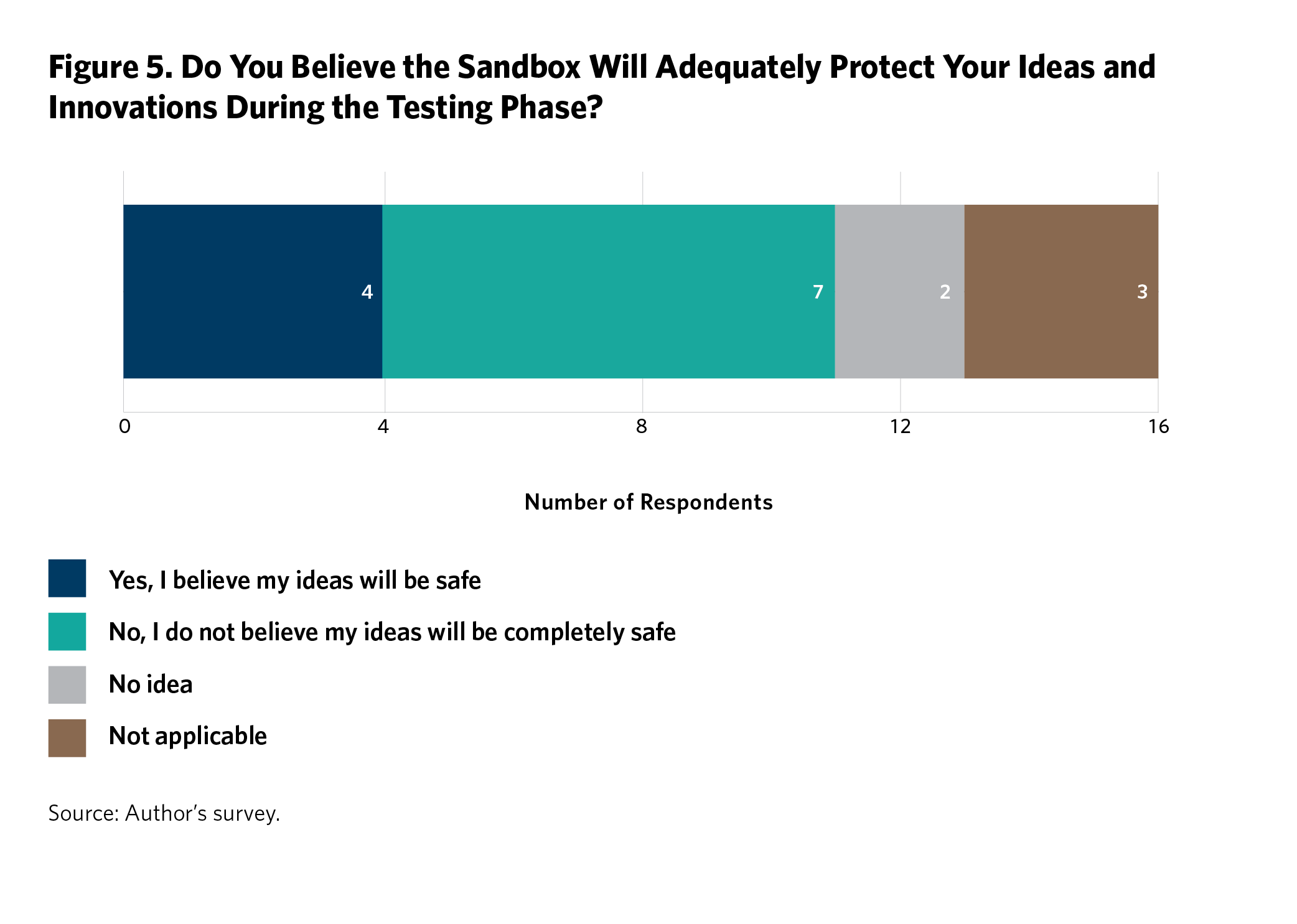

PROTECTION OF INTELLECTUAL PROPERTY

Respondents were asked how confident they were in the safety of their ideas and innovations while participating in the sandbox. Most respondents expressed their discomfort regarding information confidentiality (see figure 5).

There were some reservations regarding whether the RBZ had the internal capacity to manage the sandbox adequately. Similar sentiments were expressed regarding the confidentiality or the safety of ideas in the sandbox. To its credit, the RBZ has constituted the NFSC and Interagency Fintech Working Group (IFWG) that will oversee the development of fintech companies in Zimbabwe, including best practices and regulatory responses, and provide recommendations to the NFSC. This is a laudable step; the IFWG can detect possible conflicts of interest early while bringing a more comprehensive range of skills to the NFSC. The NFSC comprises representatives from various stakeholders, including the Ministry of Finance and Economic Development; the Ministry of Information Communication Technology and Courier Services; the Zimbabwe Revenue Authority; the Securities Exchange Commission of Zimbabwe; the Ministry of Industry and Commerce; the Ministry of Justice, Legal and Parliamentary Affairs; the Office of the President and Cabinet; the RBZ; the Insurance and Pensions Commission; and the Postal and Telecommunications Regulatory Authority of Zimbabwe.18

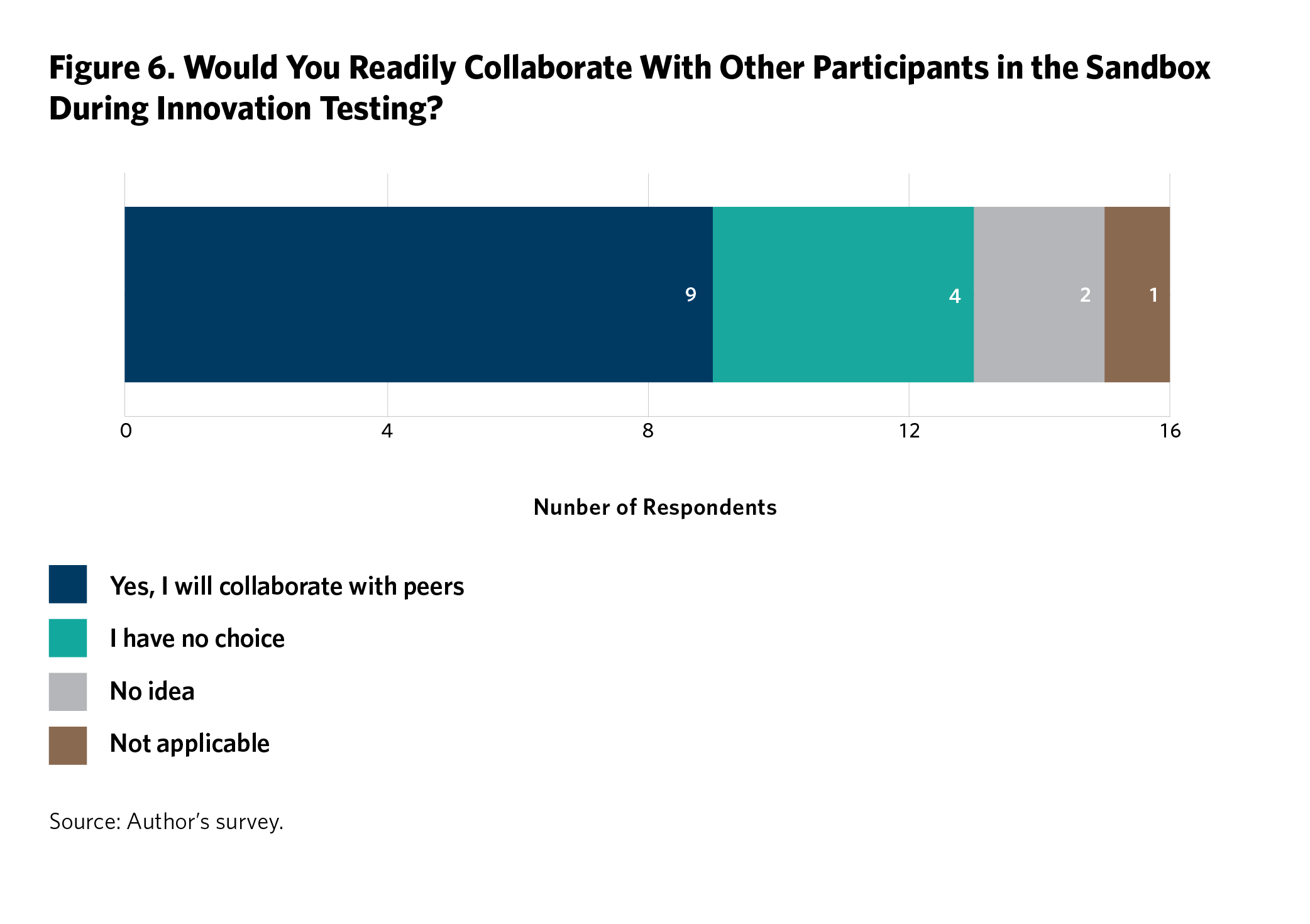

COLLABORATION

Respondents were asked whether they would readily collaborate with their peers in developing or refining their innovations. Most participants indicated they would be willing to share ideas with other sandbox participants (see figure 6).

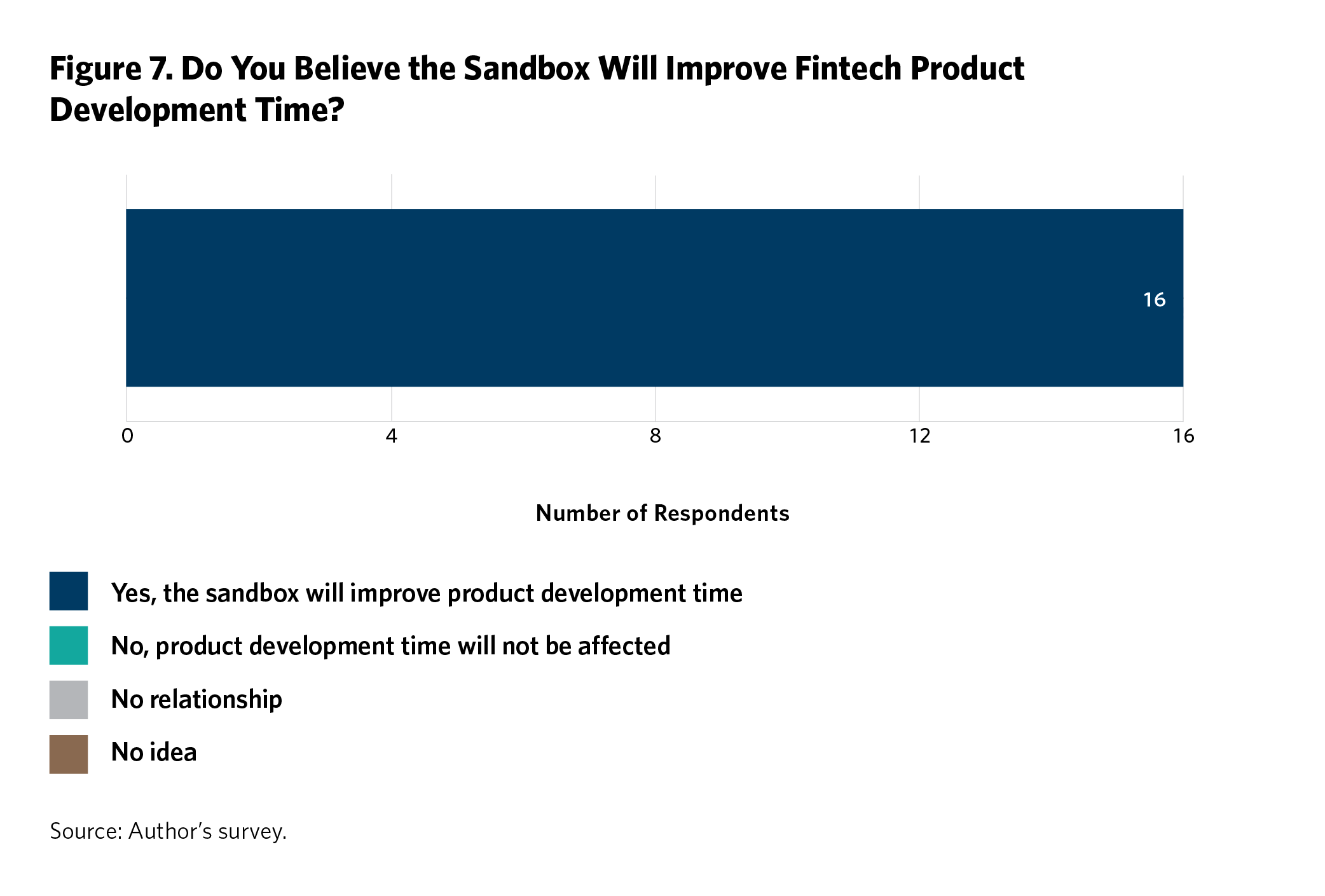

PRODUCT DEVELOPMENT

Respondents were asked whether they believed the sandbox could help reduce product development time. As shown in figure 7, all participants thought it would. They also indicated that they would be willing to collaborate with peers in developing or refining their innovations through engagement within the sandbox. Most participants believed the sandbox would assist the RBZ in monitoring fintech developments (see figure 2). These responses are good news for developing safe, innovative digital financial services and products.19

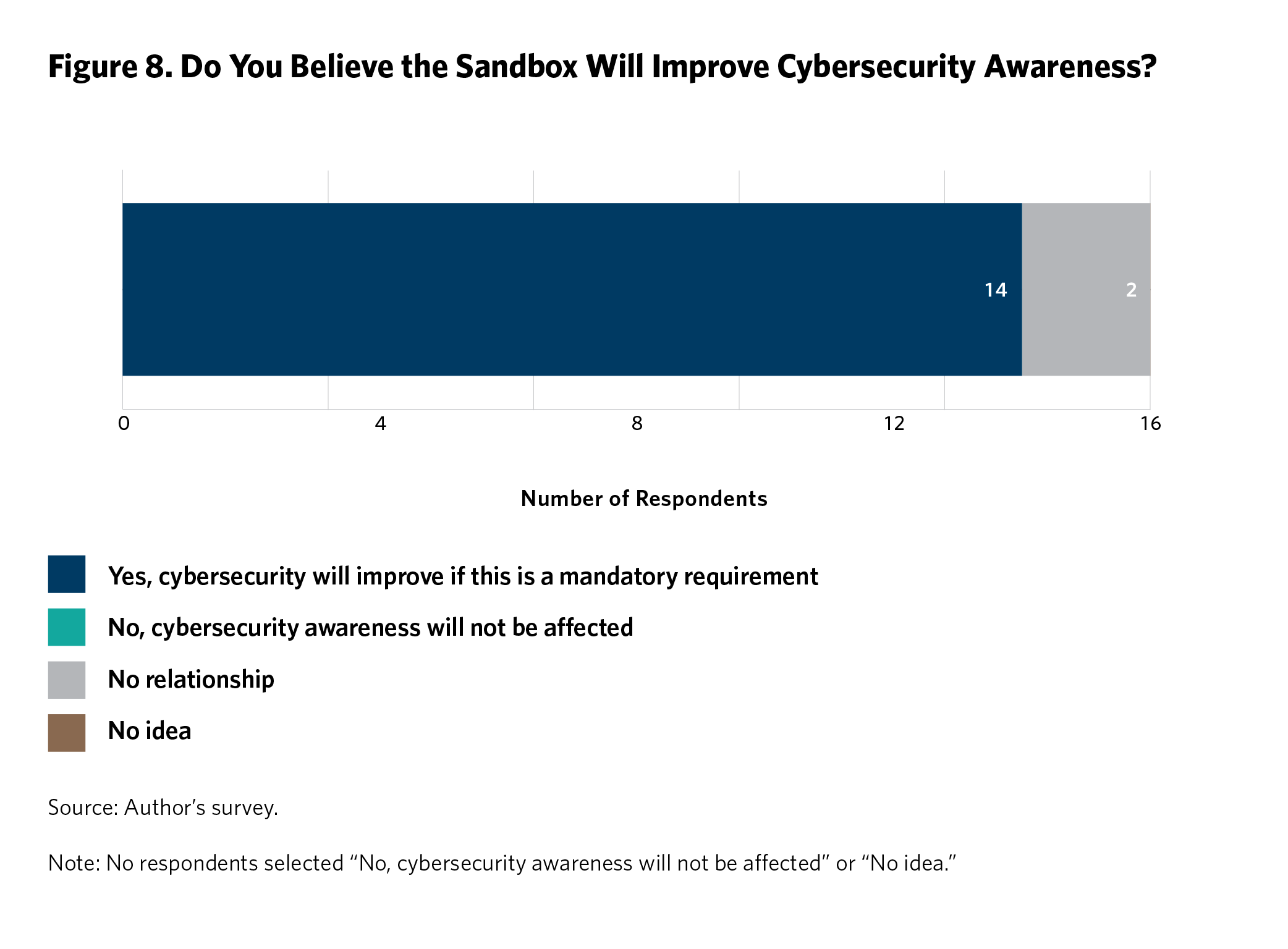

CYBERSECURITY AWARENESS

Respondents were asked whether they thought the regulatory sandboxes could be used to improve cybersecurity awareness among consumers of fintech products. As shown in figure 8, 87 percent believed this was possible only if the RBZ insisted on cybersecurity awareness before launching fintech solutions, and 13 percent saw no relationship between cybersecurity and the regulatory sandbox. Respondents were offered the option to select an answer saying that the sandbox would not affect cybersecurity awareness, but no respondents chose that answer.

Most participants saw a correlation between cybersecurity and the regulatory sandbox, but they believed the regulator needed to make cybersecurity awareness a requirement during the testing phase. Ideally, the RBZ must provide oversight on cybersecurity for fintech products and services and encourage participants to embrace the secure-by-design concept.

Managing how customer data is handled is vital because of the systemic risks that could arise from digital innovation failures.20 The supportive responses from participants should be welcome news to the RBZ and NFSC, as one of the objectives of the sandbox is to ensure the safety of fintech consumers. It is in the best interest of well-resourced, technologically savvy institutions like banks and fintech companies to overcome the competitive pressures among them and extend cybersecurity to protect consumers of financial and digital services, who may be less savvy and more vulnerable. Put simply, a robust system makes everyone safer.

CONCLUSION

This paper explored factors that could significantly impact the success or failure of Zimbabwe’s newly established fintech regulatory sandbox. The regulator and the sandbox participants hope that the sandbox will provide information on new fintech solutions in the market; identify early possible disruptive technologies that have the potential to cause systemic risk in the market; create proximity and a direct interface between the regulator and market participants; reducing development time and the time to market of solutions (saving costs); assist sandbox participants in convincing investors to fund their innovations; and bolster cybersecurity within the emergent digital financial landscape and protect consumers of fintech products and services.

The success of the regulatory sandbox, however, hinges on several factors. Key among these is quality communication with and education of the various stakeholders in the digital financial services space, which is necessary and urgent.

The government of Zimbabwe needs to stabilize the economy. While commendable progress has been achieved in financial inclusion and digital innovation, much still needs to be done. Small and up-and-coming fintech companies do not have the financial muscle to manage the frequent upswings and downswings Zimbabwe’s economy is currently experiencing; these could result in a brain drain of some of the country’s best minds.21 The notion of skill loss is aptly summed by fintech scholar Hilary J. Allen, who postulates that “the market for fintech products and services does not respect national borders, with many of these solutions being developed and deployed simultaneously in different markets.”22

The regulatory sandbox is not a novel concept and has been implemented in many jurisdictions globally. However, the success of Zimbabwe’s sandbox is yet to be adequately quantified. Whether the regulatory sandbox will succeed or fail and which areas will require refinement remains to be seen.

NOTES

1 Giulio Cornelli et al., “BIS Working Papers No. 901: Regulatory Sandboxes and Fintech Funding: Evidence From the UK,” Bank for International Settlements, 2023, https://www.bis.org/publ/work901.pdf.

2 “Fintech Regulatory Sandbox Guidelines,” Reserve Bank of Zimbabwe, accessed February 2, 2023, https://www.rbz.co.zw/documents/BLSS/Fintech/FINTECH-REGULATORY-SANDBOX-GUIDELINES.pdf.

3 “Understanding the Importance of Regulatory Sandbox Environments and Encouraging Their Adoption,” African Development Bank Group, 2022, https://www.afdb.org/sites/default/files/documents/publications/afdb_regulatory_sandbox_report_220522.pdf.

4 “Fintech Institutional Arrangements,” Reserve Bank of Zimbabwe, accessed November 22, 2023, https://www.rbz.co.zw/index.php/fintech/1066-institutional-arrangements.

5 The Financial Stability Board defines fintech as “technologically enabled financial innovation in financial services that could result in new business models, applications, processes or products with an associated material effect on financial markets and institutions and the provision of financial services.” See “FinTech,” Financial Stability Board, May 5, 2022, https://www.fsb.org/work-of-the-fsb/financial-innovation-and-structural-change/fintech/.

6 “Monetary Policy Statement: Strengthening the Multi-Currency System for Value Preservation & Price Stability,” Reserve Bank of Zimbabwe, October 1, 2018, https://www.rbz.co.zw/index.php/publications-notices/notices/press-release/568-monetary-policy-statement-01-october-2018.

7 “Zimbabwe,” World Bank Data, accessed May 1, 2023, https://data.worldbank.org/country/ZW.

8 “Zimbabwe Fintech Ecosystem Study,” Financial Sector Deepening Africa, March 25, 2020, https://www.fsdafrica.org/wp-content/uploads/2020/03/Zim-Fintech-Report-25.03.20_FINAL.pdf.

9 Wolf-Georg Ringe and Christopher Ruof, “Regulating Fintech in the EU: the Case for a Guided Sandbox,” European Journal of Risk Regulation 11, no. 3 (September 2020): 604–629.

10 Dirk A. Zetzsche, Ross P. Buckley, Janos N. Barberis, and Douglas W. Arner, “Regulating a Revolution: From Regulatory Sandboxes to Smart Regulation,” Fordham Journal of Corporate and Financial Law 23, no. 1 (2017): 31.

11 Reserve Bank of Zimbabwe, “Regulatory Sandbox Guidelines.”

12 “Press Statement Warning Against Trading in Cryptocurrencies,” Reserve Bank of Zimbabwe, May 2018, https://www.rbz.co.zw/documents/BLSS/BANK%20SUPERVISION/Press%20Releases%20&%20Speeches/2018/PRESS%20STATEMENT%20ON%20WARNING%20AGAINST%20TRADING%20IN%20CRYPTOCURRENCIES%20%20%20-%2011%20May%202019.pdf.

13 John Panonetsa Mangudya, “Monetary Policy Statement: Stay the Course,” Reserve Bank of Zimbabwe, February 7, 2022, https://www.rbz.co.zw/documents/mps/2022/Monetary-Policy-Statement-February-2022.pdf.

14 Mangudya, “Stay the Course.”

15 John Panonetsa Mangudya, “Mid-Term Monetary Policy Statement: Restoring Price and Exchange Rate Stability,” Reserve Bank of Zimbabwe, August 11, 2022, https://www.rbz.co.zw/documents/mps/2022/Monetary-Policy-Statement-August-2022-.pdf.

16 “Zimbabwe National Financial Inclusion Journey 2016-2020,” Reserve Bank of Zimbabwe, 2021, https://www.rbz.co.zw/documents/BLSS/2021/FINANCIAL-INCLUSION–JOURNEY.pdf.

17 Tunyathon Koonprasert and Ali Ghiyazuddin Mohammad, “Creating Enabling Fintech Ecosystems: The Role of Regulators,” Alliance for Financial Inclusion, https://www.afi-global.org/sites/default/files/publications/2020-01/AFI_FinTech_SR_AW_digital_0.pdf.

18 Reserve Bank of Zimbabwe, “Fintech Institutional Arrangements.”

19 Marta Barroso and Juan Laborda, “Digital Transformation and the Emergence of the Fintech Sector: Systematic Literature Review,” Digital Business 2, no. 2 (2022): 100028, https://doi.org/10.1016/j.digbus.2022.100028.

20 Koonprasert and Mohammad, “Creating Enabling Fintech Ecosystems.”

21 Financial Sector Deepening Africa, “Zimbabwe Fintech Ecosystem Study.”

22 Hilary J. Allen, “Sandbox Boundaries,” Vanderbilt Journal of Engineering and Technology Law 22 (2019): 299, https://ssrn.com/abstract=3409847.

Source link : https://carnegieendowment.org/research/2024/02/sandbox-or-quicksand-an-analysis-of-zimbabwes-fintech-regulatory-sandbox

Author :

Publish date : 2024-02-07 08:00:00

Copyright for syndicated content belongs to the linked Source.