In June, the European Parliament voted to effectively outlaw the sale of new cars using gasoline or diesel by 2035. If approved by the European Union, the move would revolutionize the world’s third-largest auto market after China and the United States—and hasten the global transformation of the entire automotive industry to battery technology.

What the parliamentarians didn’t mention: The world cannot mine and refine the vast amounts of minerals that go into batteries—lithium, nickel, cobalt, manganese, palladium, and others—at anywhere close to the scale for this rapid transition to electric vehicles (EVs) to occur. The dirty secret of the green revolution is its insatiable hunger for resources from Africa and elsewhere that are produced using some of the world’s dirtiest technologies. What’s more, the accelerated shift to batteries now threatens to replicate one of the most destructive dynamics in global economic history: the systematic extraction of raw commodities from the global south in a way that made developed countries unimaginably rich while leaving a trail of environmental degradation, human rights violations, and semipermanent underdevelopment all across the developing world.

Some countries are trying to buck this trend and get a bigger share of energy transition riches. Indonesia, for example, introduced a ban on the export of raw nickel ore in 2020, effectively forcing foreign companies to relocate their nickel processing to Indonesia. But many economists question whether such bans actually spur development. In a competitive global market, such initiatives are frequently stymied by a lack of local skills and logistics networks. Bolivia similarly attempted to add value to its lithium reserves, with only lackluster results so far.

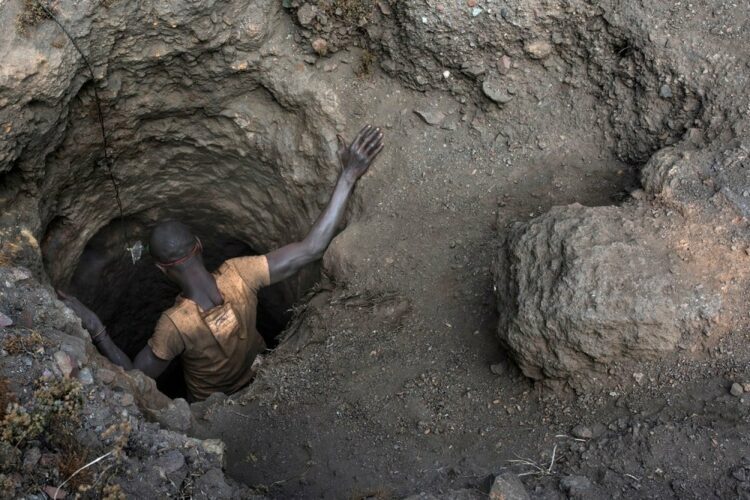

But it’s not just economics. As battery metals take on a strategic significance in many ways similar to the central role long played by oil, it will be very hard for developing countries with significant resources to keep their development trajectories from being hijacked by geopolitics. No country illustrates that problem better than the Democratic Republic of the Congo, which controls the world’s largest known reserves of cobalt—a metal that has emerged as key to the green transition, not least because EV batteries produced with cobalt tend to allow longer driving distances between charges.

Enter China, whose government identified EV batteries and their supply chains as a strategic industrial niche early on. In 2016, when the cobalt price was relatively low, Beijing went on a shopping spree. The mining giant China Molybdenum bought one of the world’s largest cobalt mines, Tenke Fungurume, located in southeastern Congo, from the U.S. company Freeport-McMoRan. Today, Chinese companies control 60 percent of global cobalt reserves and 80 percent of the world’s cobalt refining capacity, which has helped China secure a significant lead as an EV battery maker. A single Chinese company, CATL, controls one-third of the entire global battery market.

China’s targeting of batteries as part of its strategic industrial planning has spurred anxiety in the United States. In May, the Biden administration announced a $3 billion plan to boost the domestic production of EV batteries. But for any attempt to wrest a larger part of the battery supply chain from China to succeed, U.S. manufacturers will also need greater access to minerals such as cobalt. This has put Congo—and Chinese activities there—into Washington’s crosshairs.

Congo is no ordinary African country. Roughly the size of Western Europe, Congo and its vast resources are in many ways key to the economic fortunes of the entire African continent. Any partner with an eye on Congo’s mineral wealth would have to overcome the same hurdles holding back the continent as a whole. Because of Congo’s vast size, virtually landlocked position at the center of Africa, and poor access to transportation hubs, any systematic development of Congo’s resources would radiate to neighboring countries and set precedents, good and bad, for the rest of the continent.

A key issue is cross-border infrastructure such as railways and access to seaports. This is not just a prerequisite for bringing battery resources to market. The dearth of cross-border infrastructure in much of Africa also means that efforts to integrate the continent’s economies have never really taken off, even though the African Continental Free Trade Area, created in 2018, is the world’s largest free trade zone, at least on paper, encompassing 43 states. Here, China is far ahead, with rail and port infrastructure funded and built by Chinese entities transforming African logistics. In 2019, the Center for Strategic and International Studies estimated that 46 sub-Saharan African ports were built, expanded, or operated by Chinese entities.

The combination of rail and port infrastructure is potentially powerful. For example, the Atlantic Ocean port of Lobito in Angola was recently connected via an 830-mile rail line to the southern border of Congo. Several East African countries are also competing for the funding to connect their Indian Ocean ports to eastern Congo. But as various Chinese entities with various commercial and political interests focus on connecting resource-producing areas to the sea for onward shipment to China, they end up, on a broader level, replicating the resource extraction economy of the colonial era—a situation that puts a country like Congo at risk of staying stuck in perpetual underdevelopment. The more hopeful view is that once in place, cross-border infrastructure will open alternative options for development, such as boosting intra-African trade and local manufacturing.

Chinese miners have been accused of worsening what were already low labor and environmental standards, and there is ample proof of bad practices among Chinese entities in Congo. Chinese companies have also been slow in delivering promised infrastructure projects that were part of major minerals deals but not directly related to the extraction economy—such as schools, hospitals, and other social infrastructure.

Some see this as an opportunity for Western companies to displace their Chinese competitors by striking deals with Congo that have a greater development focus. Over the last few years, joint delegations of U.S. government officials and corporate executives, as well as European groups, have visited Congo, but there have been few public announcements of concrete cooperation agreements.

But even if China were to face greater competition for Congo’s favors, that’s no guarantee the energy transition won’t set off another scramble for African resources with few benefits for most Africans. That’s because the West hasn’t been demonstrably better than China. Western giants operating in Congo, such as the Swiss mining and commodity trading company Glencore, have a long and ongoing record of human rights violations and corruption. A quick look at Western history in Congo—from Belgium’s horrific colonial reign to U.S. support for the notoriously brutal and corrupt regime of Mobutu Sese Seko—makes it hard to paint Chinese investors as somehow uniquely bad among the foreign actors operating in Congo.

If anything, China and the West are pulling the same string: In 2018, China Molybdenum joined forces with Western companies such as Glencore and Ivanhoe Mines to oppose a new mining code that increased the Congolese government’s share of mining royalties. The ensuing wrestle between the government and companies included a temporary halt on China Molybdenum’s operations. But the company has powerful allies within the government that complicate any efforts to reform the country’s mining sector—if that’s indeed the government’s aim, since Congolese politics are highly corrupt and shadowy at best.

But even if U.S.-Chinese competition could raise Congo’s leverage, it may be difficult to get more U.S. companies interested in Congo. With investors increasingly focused on compliance with environmental, social, and governance standards, many companies are loath to do business in a notoriously corrupt country like Congo. There are legal constraints as well, such as the Foreign Corrupt Practices Act, which has no equivalent in China.

Washington discourse often frames the issue as if Africa’s future prosperity depends on its choice of partners, with the United States presented as the more ecologically responsible, transparent, and development-minded actor. In reality, the United States and China may be much closer to each other than this narrative makes them out to be. Both are focused on extracting raw ore and preferably refining it at home. While they might locate more refining capacity in Congo if pushed—thus leaving Africans with a larger share of mineral profits—this would be nowhere near what it actually takes for Africa to become prosperous from its mineral wealth. The entire logic of the battery metals race is to secure national prosperity at home—not in Africa. The holy grail of Africa’s economic development is the construction of its own manufacturing base—if necessary, with the forced transfer of intellectual property so that companies not only extract and refine metals but relocate the entire battery supply chain. Right now, that remains a pipe dream—not least because manufacturing requires a stable electricity supply, which is already a tall order for countries such as Congo.

In the end, the race between Washington and Beijing for EV battery minerals papers over the deep and fundamental gulf not between China and the United States but between North and South. For the global south to actually benefit in a broad-based and comprehensive way from its vast mineral wealth—resources that have become existential for climate policy—it would take such overwhelmingly massive changes in global supply chains and economic relations that they tend not to be articulated at all.

Source link : https://foreignpolicy.com/2022/06/30/africa-congo-drc-ev-electric-vehicles-batteries-green-energy-minerals-metals-mining-resources-colonialism-human-rights-development-china/

Author :

Publish date : 2022-06-30 07:00:00

Copyright for syndicated content belongs to the linked Source.

{kind=link}